How 2018’s Best Personal Finance Software Will Help You to Revolutionize Your Money

I love that blogging is a way to connect with others, share advice and grow. And I am also happy for the opportunity to feature other bloggers on my site. I am not a financial wiz by any means, however, I am excited that Kelley is willing to share her financial expertise with us. Below Kelley shares how using technology can help you pay off debt, avoid future debt and start to build wealth using the best personal finance software of 2018. Today’s technology makes it possible to organize your finances and keep track of your spending so easy and convenient! I’m so happy to share Kelley’s tips and advice below.

Using Technology to Revolutionize Your Money

There’s no question technology has improved our access to money. From credit cards to Apple Pay, spending money is incredibly easy nearly anywhere in the world.

But spending money creates an equally troublesome problem…

Spending money we don’t have becomes just as easy.

For me, spending money was so ‘easy’, I managed to grow my debt into a disastrous $77,000, spread across lines of credit, credit cards, a car loan, a student loan, and a debt owed to a friend.

After hitting my financial bottom, I managed to repay it in one year and ten months.

With the help of technology, and a plan to pay my debt, I learned to master my money, completely overhauling my approach to finances.

Through cutting-edge software, I learned to repay and avoid future debt, level my cash flow, save for unexpected expenses and build wealth.

Here, I’ll walk you through the software I used, and how you can do the same to totally revolutionize your money.

But first…

If you don’t have one…

You Really Need a Budget

I know. I know.

Budgeting sounds really scary.

I equate it to a diet of spinach, fish, and egg whites.

On first glance, it’s dull and restrictive.

But, done right, it has the capacity to completely overhaul your finances.

Tell me something?

Do you ever feel overwhelmed with guilt after buying something?

Or, do you feel panicked because you don’t know how you’ll cover that really big bill?

Yup, I felt that way too.

Once I started budgeting though, that yucky feeling all but disappeared.

Why?

Because budgeting, according to people like Dave Ramsey, helps you tell your money where to go, rather than being left to wonder where it went.

Old school methods of budgeting, or cash-based budgeting, involved using something like envelopes. You’d write budget categories across them – gas, groceries, rent, etc. Then taking your paycheck, you’d divvy up your money, and put the required amount into each envelope.

The envelope system was incredibly effective, but in today’s world…

Working strictly with cash is totally IMPRACTICAL.

Challenges With Older Methods of Budgeting

Sure, there are still experts who swear by cash-based budgeting, but let’s be honest, it’s just not practical anymore.

Consider tasks like:

- Booking a flight.

- Securing a hotel.

- Paying bills.

- Paying for large expenditures, like mortgages and rent.

I could only imagine Expedia’s response to you telling them your cash envelope is in the mail!

And, besides just that, consider small errands like getting groceries and paying for gas. To do only these two things you’d likely need to haul around a few hundred dollars everywhere you go.

And, even if you don’t use cash, keeping tabs on multiple accounts and bill payments is cumbersome too.

Technology and innovation created this incredible access to money through credit cards, lines of credit, chequing accounts and more. But, the result, for most of us, is a really complex and difficult to manage, financial life.

Why Use Budgeting Software?

Ok, hopefully, we’ve established if you want to master your money, you really need a budget.

But, why should you leverage budgeting software?

Sure, you could use the ole pen and paper method, or just use excel.

In my opinion, only robust software has the capacity to eliminate financial complexity.

You might have:

- Multiple bank accounts

- Multiple credit products

- Numerous bills to pay

Great software will streamline your accounts – bringing all accounts (even those from different institutions) together. It will make your money visual – making what’s become intangible, more tangible. It will remind you of your bill due dates, provide historical data, and let you set (and achieve) your financial goals.

The Very Best in Budgeting Software

I might be slightly biased, because YNAB (or You Need A Budget) is the software I used to repay my $77,000 debt.

YNAB has a zillion features to streamline your finances. It seriously makes my money boring – I don’t have to stress or worry about anything anymore.

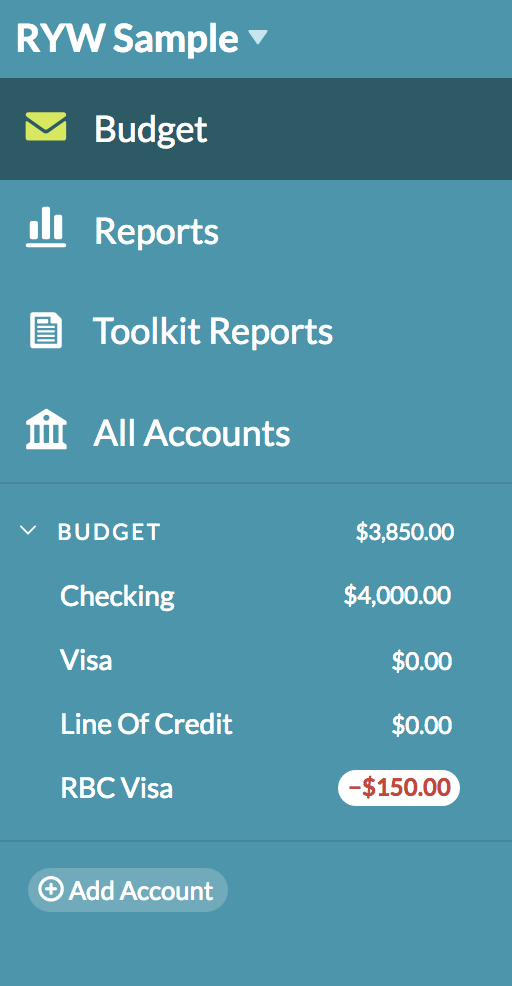

Track Your Spending

The first thing it does is track all of your spending. In the screenshot below you can see a number of sample accounts I’ve added. You’re able to add as many accounts as are relevant to you. Here’s you’d see the name of the account and the corresponding balance:

Then, as you spend, you’ll see the expenditures. Included is the place you spent the money (the payee), the category (think of it as the envelope), any notes, and the amount. In a sense, this portion of the software is tracking your spending, but the pivotal part is that each transaction is connected to your budget.

Follow Your Budget

YNAB’s budget screen is where you’re able to set up your budget categories. You can customize these anyway that suits you. To the right of the budget names, you’ll be able to ‘budget’ money. This portion of YNAB makes the old envelope system of budgeting digital.

In the example below, you can see my Grocery Category with ($300) noted as a reminder. Then, in the following column, you’ll see how much I’ve budgeted, then how much I’ve spend, and how much remains.

In the example below, if I budget $300 for groceries, and spend, $125, I have $175 remaining.

This is the most mind-bending part of YNAB’s budgeting software. Rather than relying on your bank account balance for your spending decisions, you’d begin to refer to your category balances.

For example, when thinking of buying new clothes, although my bank balance might be $2,500, my clothes category might be $0. This is because the $2,500 is already budgeted and is intended for other obligations – like rent, phone, car, electricity. Consider the $2,500 as cash divvied up into various envelopes.

Rather than feeling restrictive, you’ll start making different choices to support your financial well being.

And, similar to envelopes, if you underspend in one area, you can move the excess money somewhere else.

Viewing Historical Data

Ever wonder how much money you waste at Starbucks, or on eating out?

Using YNAB’s report screen, you’re able to see a slew of financial data.

You’re able to select specific date ranges and highlight certain categories. You’ll get real-time data about your spending.

Other Awesome Features

Ever feel scattered trying to remember when bills are due? Especially those that happen every once in a while – like property taxes, or income taxes?

With YNAB, you can enter future bill reminders, and can set recurring rules. Doing so, will save you late fees and interest charges and help you stop fretting about what’s due when.

With a quick glance, you’ll be able to see what you owe and when you owe it.

And, you’ll be able to do some ‘cash flow forecasting’. When you receive your paycheque, you’re able to see your upcoming financial obligations.

Below is an example of a few upcoming transactions. These are reflected in light grey to denote upcoming, versus actual transaction which appear bold.

So, if I got paid and wondered what and when I owe money, I could glance here and see that first I owe Cox Communications, then T Mobile, then my Landlord, and finally Mountainside Fitness. I’d allocate money for these things before prioritizing anything else.

Of course, in my budget, I have a huge pile of these upcoming transactions. If someone owes me money (and I don’t want to forget) I add it here. I add one-time, annual, quarterly, and monthly expenses too. I have a massive list of upcoming transactions.

Want to remember credit card bill due dates? Add them here.

Want to remember to look for a refund posted to your credit card? Add then here.

Getting Started with YNAB

Getting started with YNAB is a bit of a learning curve. You’ll have access to the desktop software and the related app. To speed up your data entry when getting started, you can use keyboard shortcuts – check out Sandy’s 10 Basic Computer Tips Everyone Should Know.

Since budgeting with YNAB, in 2012, I repaid $77,000 and haven’t paid a cent of credit card interest or late fees since.

YNAB is a monthly subscription, but it’ll save you the cost you pay and then some. To test it out before committing, you can use this link for an extended free trial – with no obligation.

To follow a step-by-step guide for getting started with YNAB, check out this video: Setting Up YNAB.

Author Bio:

Kelley Olinger is a professional freelance writer and blogger. She resides part-time in Victoria, BC, Canada, and part-time in Scottsdale, Arizona. When she’s away from her computer you’ll find her road cycling or hiking. Having repaid $77,000 in debt, Kelley’s passion is helping others ditch debt and embrace an abundant life through her blog, ReconcileYourWallet.

Thanks for sharing my article Sandy!!

Thank you for writing it!

Love your tips!